How to Read a Title Report (Washington)

- Ryan Palardy,

- January 22, 2026

Title reports are an often overlooked, but crucially important part of buying and selling a home. Reading and understanding title reports or “preliminary title commitments” can help ensure your home sale goes smoothly as a seller. It also protects you from walking into a legal morass and/or financial liability as a buyer.

This blog will teach you what a title report is, how they work, what they cover and, crucially, what they don’t cover. By the end, you will understand what pitfalls to avoid and how to walk into your new home, or away from your old one, with confidence.

What are exceptions on title reports?

Exceptions are recorded items—liens, easements, CC&Rs and other encumbrances—that the title insurance policy excludes from coverage. If something is listed as an exception, you’re taking title subject to it. Skim the numbered exceptions in Schedule B Part II and flag anything unusual; routine items often include property taxes and utility easements.

In King County (which includes Seattle and Bellevue), exceptions might reference local improvement district (LID) assessments or recorded shoreline easements. Ask your agent if these will affect your plans.

What does title insurance cover?

Title insurance protects against hidden title defects not listed as exceptions. Coverage typically includes unpaid liens or mortgages, forged or fraudulent documents, claims by missing heirs, clerical errors in public records and boundary disputes. If such an issue arises after closing, the insurer pays legal fees and financial losses to defend your ownership.

There are two policies: a lender’s policy (required by your bank) and an owner’s policy (optional but recommended). The owner’s policy protects your equity for as long as you own the home. In Washington, it is customary for the seller to pay for an owner’s policy at closing, which benefits the buyer.

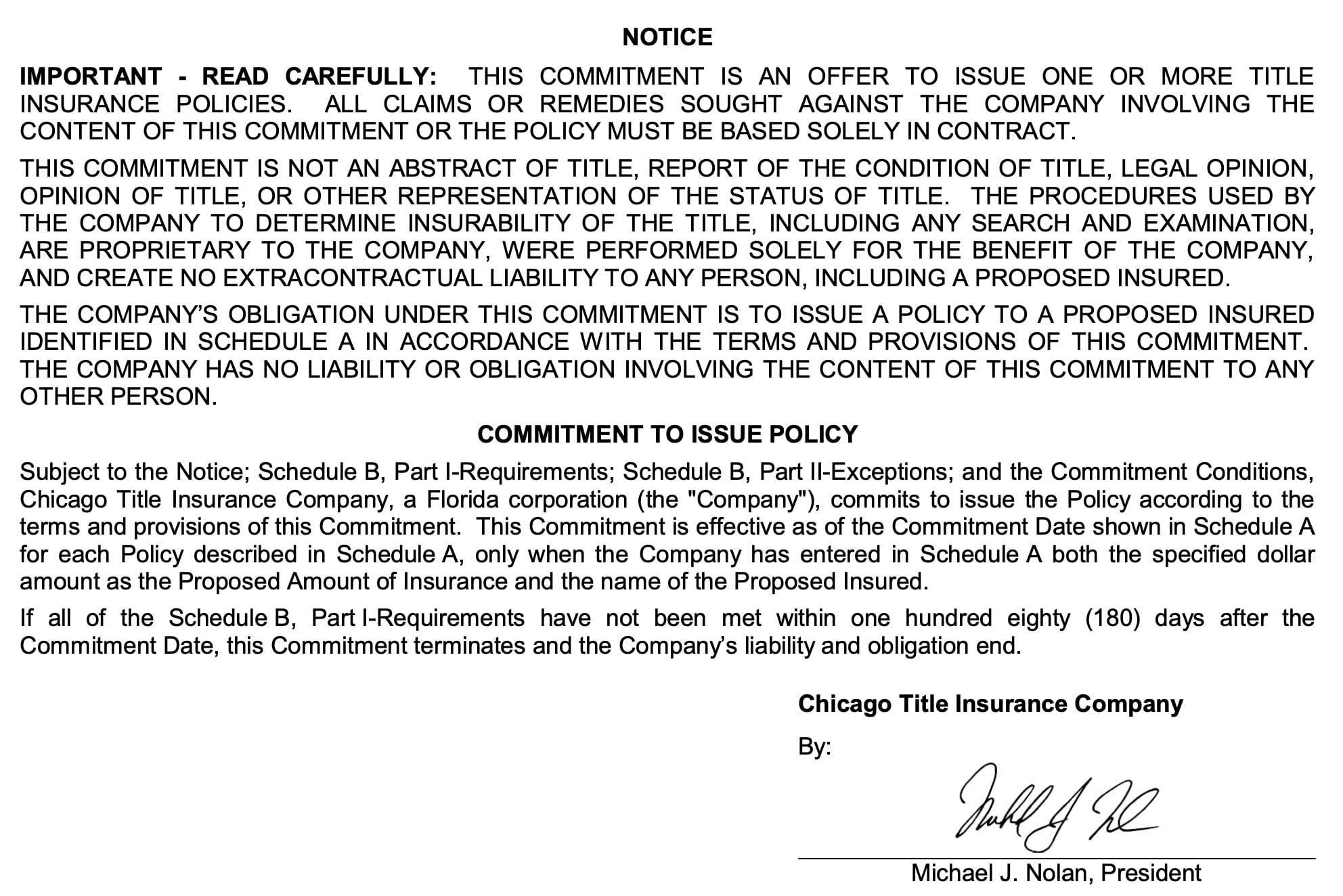

Sets expectations: the commitment is not a guarantee and is effective through a specific date. For Seattle transactions, ensure the commitment date extends beyond your scheduled closing to capture any recent recordings.

Ask: Does this commitment expire before our closing? Are there conditions that need immediate action, like probate court approval?

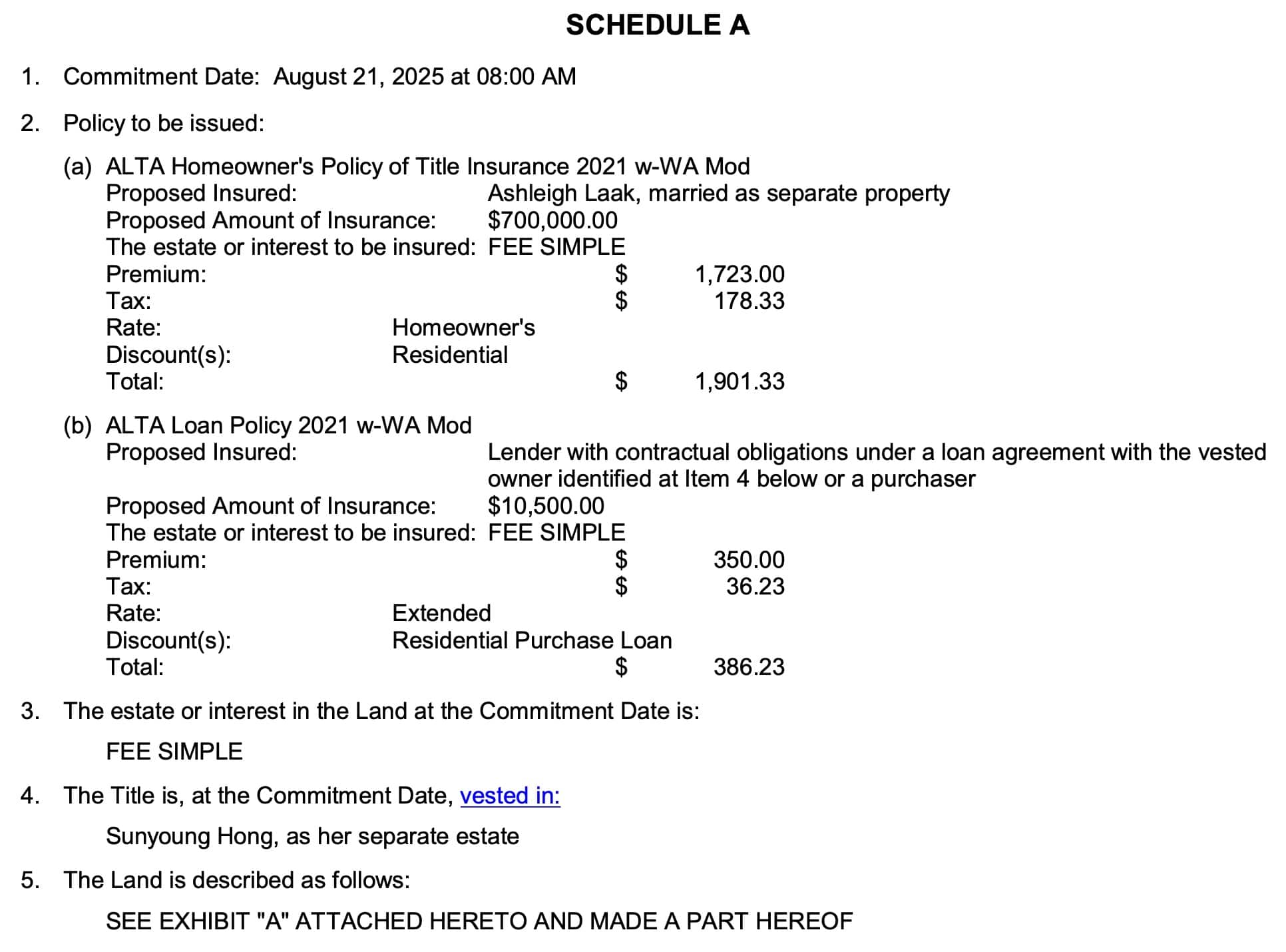

Commitment/Effective Date: The date through which King County or other county records were searched.

Policies & Amounts: Shows owner’s and lender’s policies and coverage amounts; confirm the purchase price and loan amount.

Estate & Vesting: States whether the estate is fee simple (standard ownership) and how title is vested. In Washington, married or partnered buyers often choose community property with right of survivorship.

Legal Description: Refers to Exhibit A. Make sure it matches your contract; in a condo, verify the unit number and parking spaces.

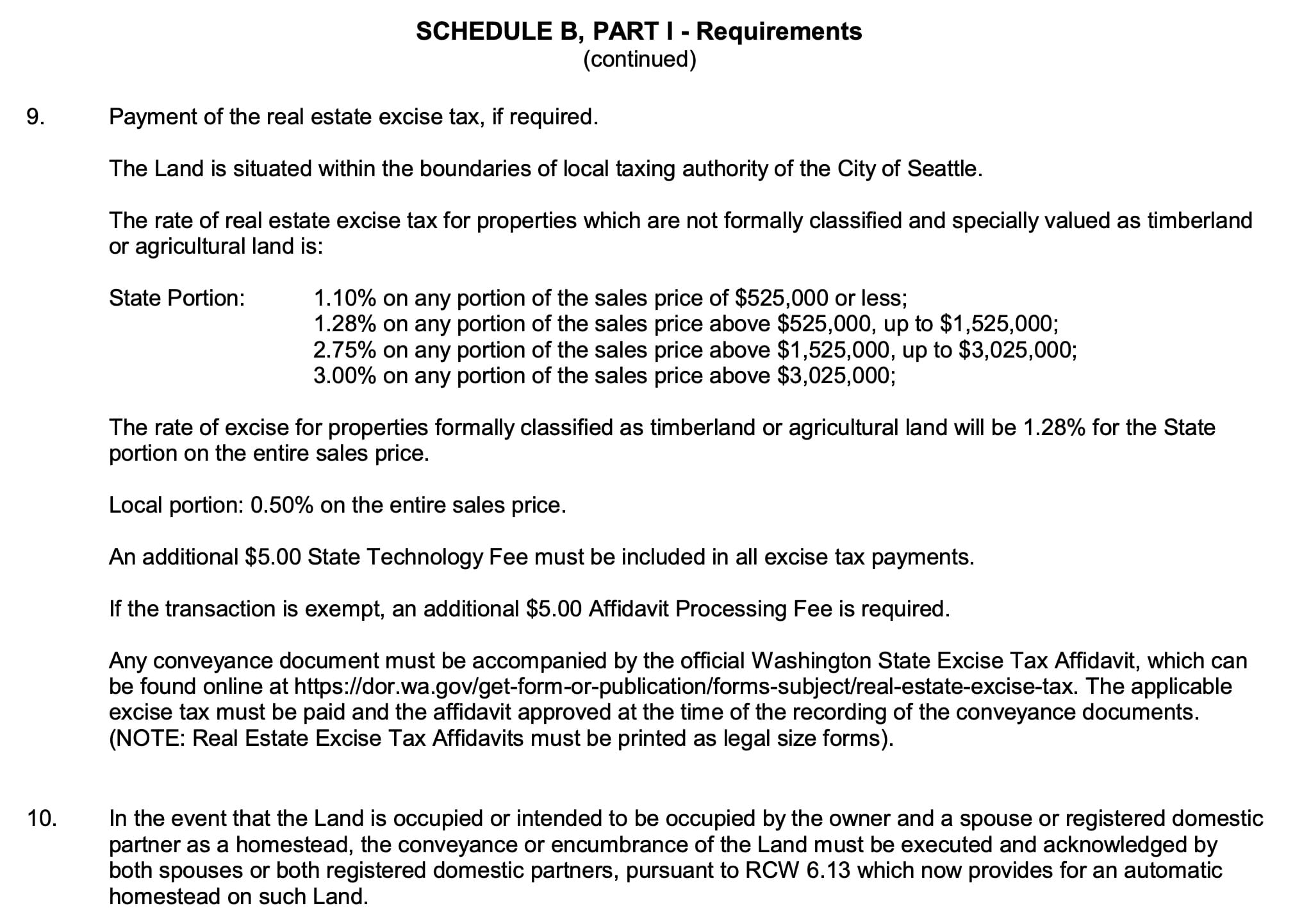

Lists conditions to clear title before issuing policies: paying premiums, recording the deed and deed of trust, releasing prior liens, paying real estate excise tax (REET) and completing affidavits. Requirements may mention FinCEN geographic targeting orders (GTOs) for cash purchases in King or Snohomish counties.

Ask: Are there any unusual requirements, such as probate or court approvals? What must we do to comply with the GTO if we’re paying cash? For more details on closing steps, refer to our guide on the escrow process in Washington.

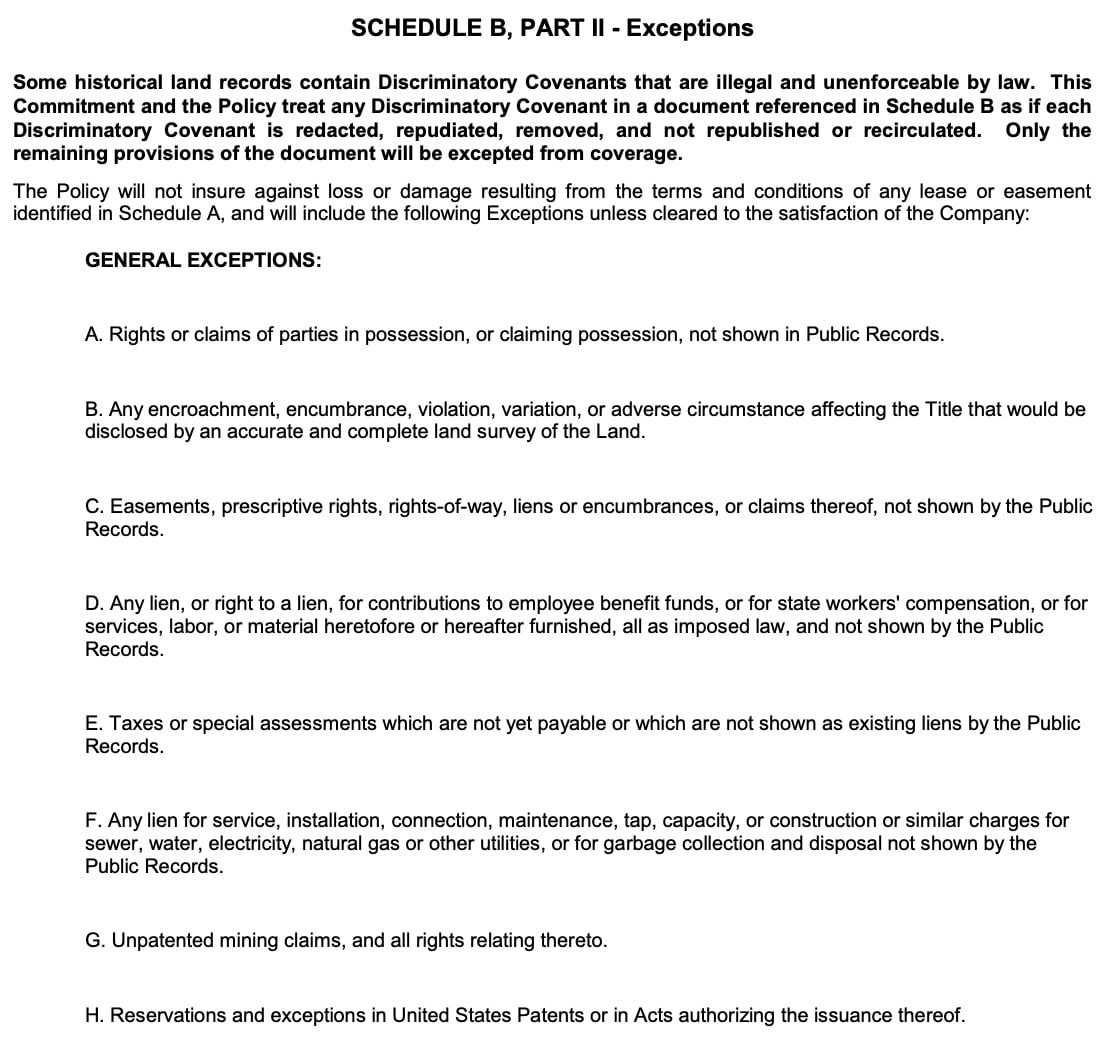

General Exceptions: Standard exclusions from coverage (survey matters, unrecorded easements, rights of parties in possession, future taxes). These can sometimes be removed with endorsements such as a survey endorsement.

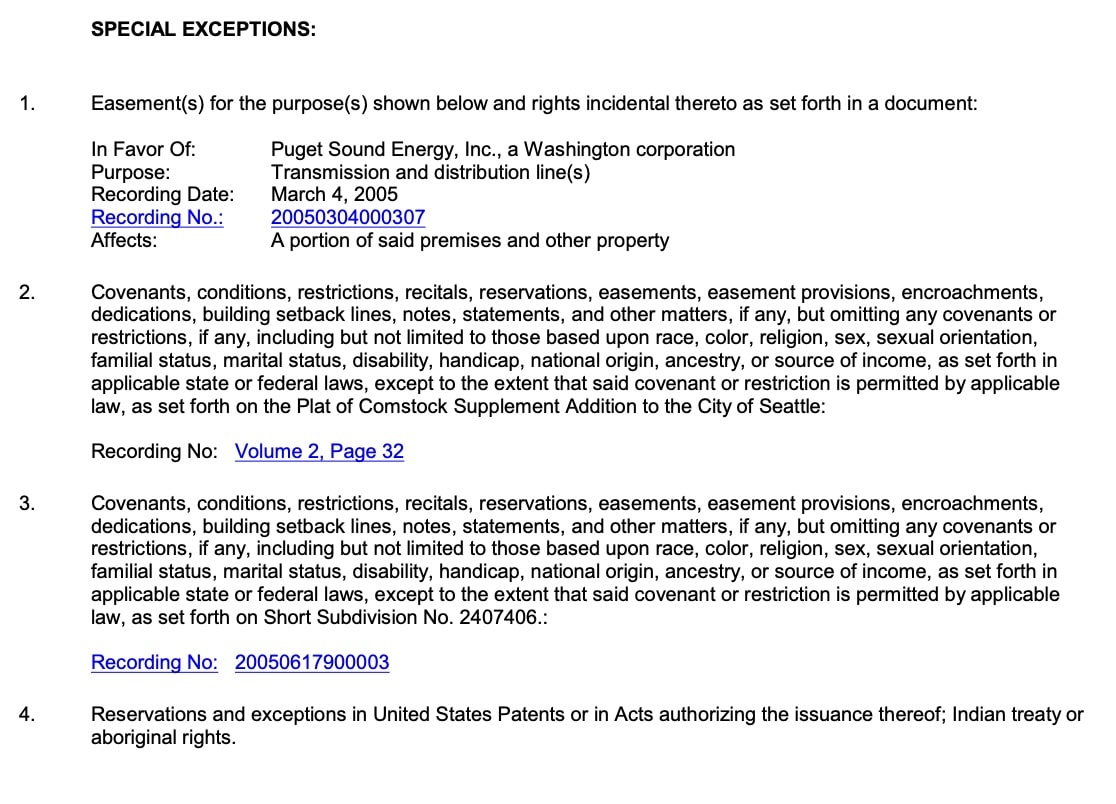

Special Exceptions: Property‑specific items that remain on title. Common categories include:

Taxes and assessments: Check for unpaid property taxes or LID assessments in Seattle or surrounding jurisdictions.

Deeds of trust/Mortgages: Existing loans recorded against the property; Washington uses deeds of trust with non‑judicial foreclosure.

CC&Rs: Subdivision covenants, HOA bylaws and condo declarations.

Easements: Utility, road and access easements; shoreline or critical area easements may appear on properties near Lake Washington or Puget Sound.

Judgments and liens: Federal tax liens, child support liens, mechanics’ liens and bankruptcy filings.

Other encumbrances: Survey encroachments, mineral reservations, private road maintenance agreements and water‑rights easements.

Ask: Which exceptions are typical in our region? Are any red flags that might hinder building a backyard cottage in Seattle? How can we remove or insure over specific exceptions?

Provides the full legal description. Double‑check that the tax parcel number (APN) matches the property on your purchase agreement. In Bellevue and Kirkland, look for recorded short‑plat numbers or condominium declarations.

May list Washington’s real estate excise tax (REET) rates, county recording fees and cut‑off times, FinCEN GTO compliance instructions and wire fraud notices. If you’re closing in King County, for example, recording cut‑off times are typically early afternoon—missing them can delay closing.

Ask: What are the county REET rates for our purchase price? Are there additional fees if the property is in an unincorporated area or near a shoreline? Our separate article on Washington excise tax explains the brackets and recent changes.

| Common/Normal Items | Red Flags & Follow‑Up |

|---|---|

| Current year property taxes not yet due | Delinquent taxes, prior‑year unpaid taxes or tax foreclosure notices |

| Standard CC&Rs and HOA declarations | HOA liens, default notices, or restrictions conflicting with your plans (e.g., short‑term rental bans in Seattle) |

| Utility easements for power/sewer | Private road easements with ambiguous maintenance obligations or exclusive easements that limit your use |

| One deed of trust securing the seller’s loan | Multiple deeds of trust, undisclosed private loans or judgment liens |

| General survey exceptions | Recorded boundary agreements showing encroachments or disputed property lines; consult a surveyor |

| Recorded setbacks and protective covenants | Encroachments into required setbacks; unpermitted ADUs flagged by the assessor |

| Notes about REET and recording deadlines | References to pending litigation, Lis Pendens, bankruptcy or probate filings |

Define important terms, emphasizing local context when relevant:

ALTA: American Land Title Association; provides standard forms for commitments and policies.

APN/Parcel Number: Identifier used by the county assessor; check it against your contract.

CC&Rs: Covenants, conditions and restrictions recorded against a property; often enforced by a homeowners’ association.

Community Property: Ownership form in Washington for married or partnered buyers.

Deed of Trust: Washington’s primary security instrument, allowing non‑judicial foreclosure.

Endorsement: Additional coverage modifying a title policy; endorsements can remove general exceptions or provide extended coverage.

Escrow: The neutral process through which documents and funds are held until closing; see our article on the escrow process in Washington.

FinCEN GTO: Federal rule requiring title companies in certain counties (including King and Snohomish) to report beneficial owners for high‑value cash purchases.

LID Assessment: Local improvement district fee levied to fund neighborhood projects like sidewalks or sewers; common in Seattle redevelopments.

Real Estate Excise Tax (REET): Transfer tax levied by Washington and local jurisdictions; rates vary by price bracket.

Special Exceptions: Property‑specific exclusions listed in Schedule B Part II.

Survey: Measurement of property boundaries; needed to remove survey exceptions.

Why does the report list my HOA’s CC&Rs as an exception?

CC&Rs govern how you can use the property; they remain on title and are not covered by insurance. Read them to ensure they don’t restrict planned improvements.

Can exceptions be removed?

Some can. Liens and old deeds of trust can be paid off; survey exceptions may be removed with a new survey; CC&Rs and easements typically remain. Your title officer can advise on possible endorsements.

Does title insurance cover missing heirs or forged documents?

Yes—provided these issues weren’t listed as exceptions. Title insurance pays legal fees and losses if a hidden heir or fraudulent deed is discovered.

Will my policy cover boundary disputes in Bellevue?

Many policies cover legal costs and surveys needed to resolve boundary disputes if the encroachment wasn’t disclosed as an exception.

Do I need an owner’s policy in Washington?

An owner’s policy protects your equity and lasts for as long as you own the home. While sellers often pay for it in Seattle and King County, the cost is negotiable.

What does title insurance not cover?

Known exceptions, zoning or land‑use violations, environmental hazards, and issues arising after the policy date (like new liens you incur) are not covered. Homeowners insurance covers physical damage; title insurance covers defects in ownership.

Clarify exceptions:

“I’m looking at Schedule B and see easements and a deed of trust. Can you explain what each means for our plans to add an ADU in Bellevue, and whether any can be removed or insured over?”

Explore coverage:

“If a missing heir or unpaid lien surfaces after closing, will my owner’s policy cover the legal fees and any financial losses? Are there endorsements we should consider for extra protection?”

Ask about excise tax and escrow:

“Can you confirm the real estate excise tax rate for our price bracket? Also, what are the key steps in the escrow process in Washington that we should be aware of?”

A preliminary title report is more than paperwork—it’s your roadmap to understanding a property’s history and spotting any hidden complications. In our fast‑moving Seattle and Eastside market, reviewing this report early helps you get ahead of potential issues and gives you peace of mind when it’s time to sign. Take a close look at the exceptions and understand what your title policy actually covers, and don’t hesitate to involve your real estate agent or a title professional if something isn’t clear.

If you’d appreciate a personalized walk‑through of your report, please reach out. I’m always happy to help you interpret the details and flag any items that could affect your plans. And if you’d like to learn more about HOW ESCROW WORKS or how real estate excise tax is calculated in Washington, our related guides can walk you through those topics, too. Together, we can make sure your path to “happy at home” in Seattle or Bellevue stays smooth and stress‑free.

About the Author: Ryan Palardy

About the Author: Ryan PalardyRyan Palardy is a CRS (Certified Residential Specialist) Real Estate Broker & Attorney who helps buyers and sellers move through Seattle’s housing market with strategy, confidence, and a clear understanding of what truly drives value. As part of the Get Happy at Home team, he brings the weight of more than 25 years of combined experience, $600 million in closed sales, and the trust of 1,300+ clients across Seattle and the Eastside.

Ryan’s work centers on first-time buyers, out-of-area relocations, tech employees, and homeowners preparing for a pre-sale remodel. He and the Get Happy at Home team were named Best Real Estate Team in the Seattle Times “Best in the Pacific Northwest” awards for 2025, and are known for consistently delivering top-of-market results for their sellers. The team has earned hundreds of five-star reviews across every major platform—reflecting a long-standing commitment to candor, preparation, and client advocacy.

Before real estate, Ryan practiced law in Washington after earning his J.D. from the University of Washington and receiving his WSBA license in 2018. That background shows up in the way he structures deals, spots risks early, and protects his clients’ interests. Ryan lives in Northwest Seattle with his family.

If you’re exploring a move, planning ahead, or want a clearer read on your options, you can reach Ryan directly—or connect on LinkedIn for ongoing Seattle market insights.

License info: Licensed Real Estate Broker in WA, License #21024995. Office: Seattle, WA.

This information is for educational purposes only and does not constitute legal advice. Real‑estate laws and title insurance rules can change; consult a qualified attorney or title professional for specific guidance.